With the focus topic “Performance and Perspectives of the 2nd Pillar”.

Switzerland is still a nation of savers, says Fabio Pellizzari – despite persistently low interest rates. The Head of Index Solutions now outlines which instruments may be suitable for those looking to start investing.

Find out here how to successfully enter the world of investing.

Precision, continuity, stability and security. With these Swiss qualities, we develop and manage our fund products as the second largest fund manager in Switzerland.

The importance of sustainability for our future has been incorporated in our product range since 1998. Back then, we launched the first sustainable investment product. Today, we pursue a binding CO2e reduction target in all active traditional investment funds.

Swisscanto investment funds regularly win national and international awards for their strong performance, sustainability and continuity.

Opt for a private pension in the form of securities savings. Compared to 3a account savings, the potential returns are higher in the long term.

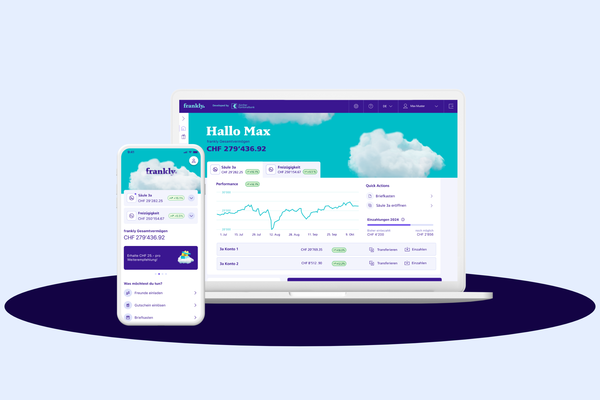

Open a frankly pillar 3a or vested benefits account and receive a CHF 35 voucher off your fees as a new client with the code SWC35

Invest as sustainably as you want. Our sustainable investment funds meet different sustainability requirements and can increase return opportunities.